|

| Chart 1 (Click on image to expand) |

According to Mr Carney, the most effective way to remedy this situation without hindering economic growth would be for Canadian businesses to increase their level of investment in upcoming years. The intended objective of increasing corporate investment is to offset the gap in the economy that is likely to occur as a result of increased household deleveraging during the next few years.

One commentator applauded Mr Carney for being the only government official at the moment to "speak the truth", that is, to tell Canadians the true state of the country's economy and exhort businesses to take this opportunity to improve their productivity and competitiveness by investing in their operations.

Still, there remains one 'truth' that has yet to be mentioned by anyone, including Mr Carney. And that is the fact that the federal government's commitment to balance its budget is highly incompatible with the objective of seeking to eliminate the household sector's net financial deficit.

To be sure, Mr Carney did mention in his speech that one way to reduce the deficit of the household sector is for governments to increase spending. But given that the speech later implies that this option is not sustainable, it is hard to tell whether Mr Carney would actually endorse the view that government deficit reduction at this time is an impediment to reducing the net financial deficit of the household sector.

The notion that government deficits have a positive effect on the financial balance of the household sector may sound like a far-fetched economic theory. But, in the case of Canada, as I have demonstrated previously, it is a well-supported empirical fact that is statistically (and intuitively) significant.

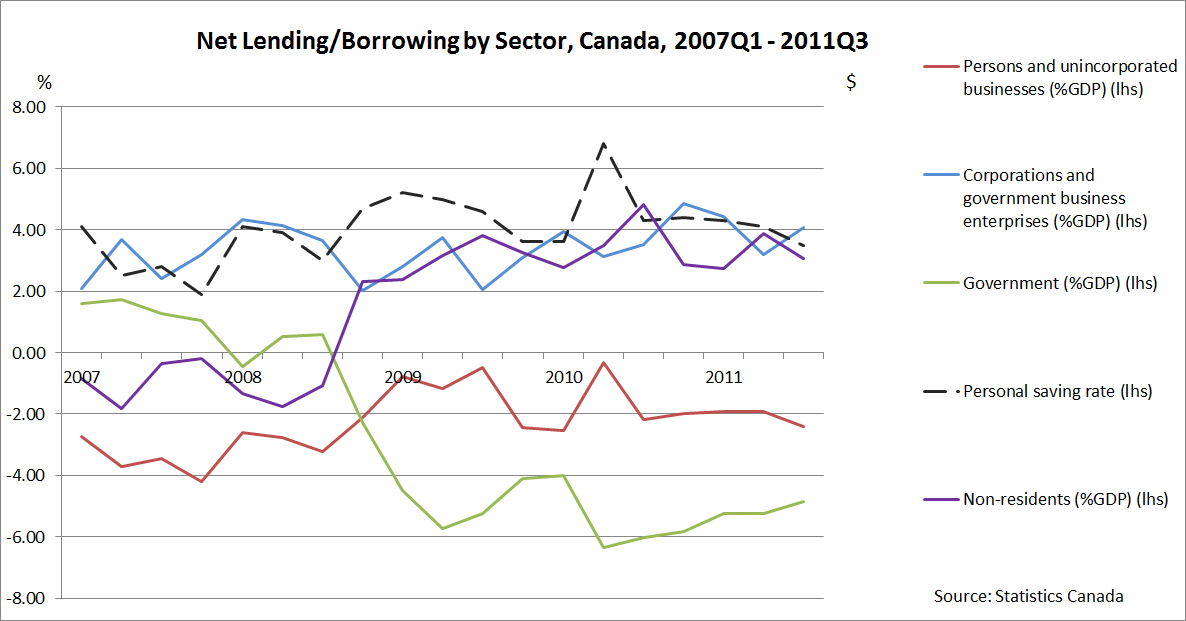

As you can see from Chart 2 below, based on Statistics Canada's sectoral net lending figures dating from 1961 to present, there is a strong relationship between the (consolidated) government deficit and the net financial surplus of the household sector. The reverse is also true, as government surpluses tend to be associated with household sector deficits.

|

| Chart 2 |

The only important exception to this longstanding economic reality surfaced in 2008 when the net financial position of the government sector fell back into a deficit (after several years of surpluses) as a result of the sharp drop in Canadian exports, a situation that enabled the foreign sector to return to a considerably large surplus position (see Chart 3). And against the backdrop of a massive and persistent corporate sector net financial surplus starting in the year 2000, the current government sector's deficit has not proven sufficiently large to return the household sector to its traditional net financial surplus position (see Chart 3).

|

| Chart 3 |

First of all, although it now appears likely that the federal government may be headed in that direction, the federal and provincial governments should immediately abandon or, at a minimum, postpone their plans to reduce their deficits and/or balance their budgets. At present, as explained above, the government deficit is actually enabling the household sector's net financial deficit from increasing any further.

Second, governments should take immediate steps to cut down on public expenditures that result in an outflow of funds away from the Canadian economy. As the above analysis suggests, large scale spending on foreign goods has the effect of both increasing the surplus of the foreign sector while simultaneously increasing the size of Canada's public sector deficit. In this regard, there is a strong case to be made for the federal government to cancel its planned purchase of American-made fighter jets.

Similarly, provincial and local public transit authorities should aim, as much as possible and in a manner consistent with established principles of economy and efficiency, to purchase equipment produced in Canada. It should be stressed that the cost-efficiency criterion for choosing among different bids for these public works projects should not be cast aside so as to ensure minimal impact on the tax burden imposed on households and businesses.

Third, as recommended in a previous column, the government should encourage firms to undertake productive investment by imposing a small, yet noticeable tax on retained earnings or on the turnover of corporate financial instruments. These measures would create incentives for firms to reinvest their profits in business operations by increasing the cost of undertaking unproductive activities (e.g., speculative investment) with profits.

Finally, the federal government should reconsider the decision taken in 2008 of requiring the Employment Insurance (EI) fund to balance within a given period. As it stands, when the fund goes into a deficit (as it has been since 2008 due to the rise in unemployment), the government must seek to eliminate the deficit in the short- to medium-term by increasing employer and employee contributions. While such a mechanism may help to reduce the size of the government deficit, it should be emphasized that this policy is highly pro-cyclical given that it acts as an impediment to reducing the net financial deficit of the household sector by decreasing the disposable income and purchasing power of households at a time when they most need it.

To conclude, Mr Carney was right in highlighting the urgency of addressing the current net financial deficit of the household sector. However, it is similarly urgent for government officials in Canada to realize that the objective of balancing public sector budgets is self-defeating and will make matters worse for households given that it reduces a source of employment and revenue. Now, it is very likely that officials of the Bank of Canada are aware of this fact but feel it is not their role to make such an observation. The purpose of the above analysis is a modest attempt to get the word out. Such is my hope and recommendation for 2012. So, on that note, I leave the reader with an excerpt of a letter by John Kenneth Galbraith addressed to President John F. Kennedy dated March 1959 summarizing the point of this column quite nicely:

I have always found that the most useful answer to [those who believe the government must balance its budget] is that the Federal Government, by unbalancing its budget, can help the man who needs a job balance his budget. (1998:29)

* A sector's net financial balance is the difference between its quarterly sectoral savings and investment as a share of gross domestic product. The sum of all sectoral balances must add to zero, which explains why the surplus of one sector is always offset by the deficit of at least one other sector.

References

Eisner, R., How Real is the Federal Budget? (New York: Free Press), 1986

Galbraith, J.K., Letters to Kennedy (ed. James Goodman) (Boston: Harvard University Press), 1998

Godley, W. and A. Izurieta, "The US economy: weaknesses of the strong economy", PSL Quarterly Review, vol. 62, nn. 248-251 (2009), 97-105

Seccareccia, M., "Growing household indebtedness and the plummeting saving rate in Canada: an explanatory note", Economic and Labour Relations Review, Vol. 16, no. 1, July, 2005, pp. 133-51